Image source: Getty Images

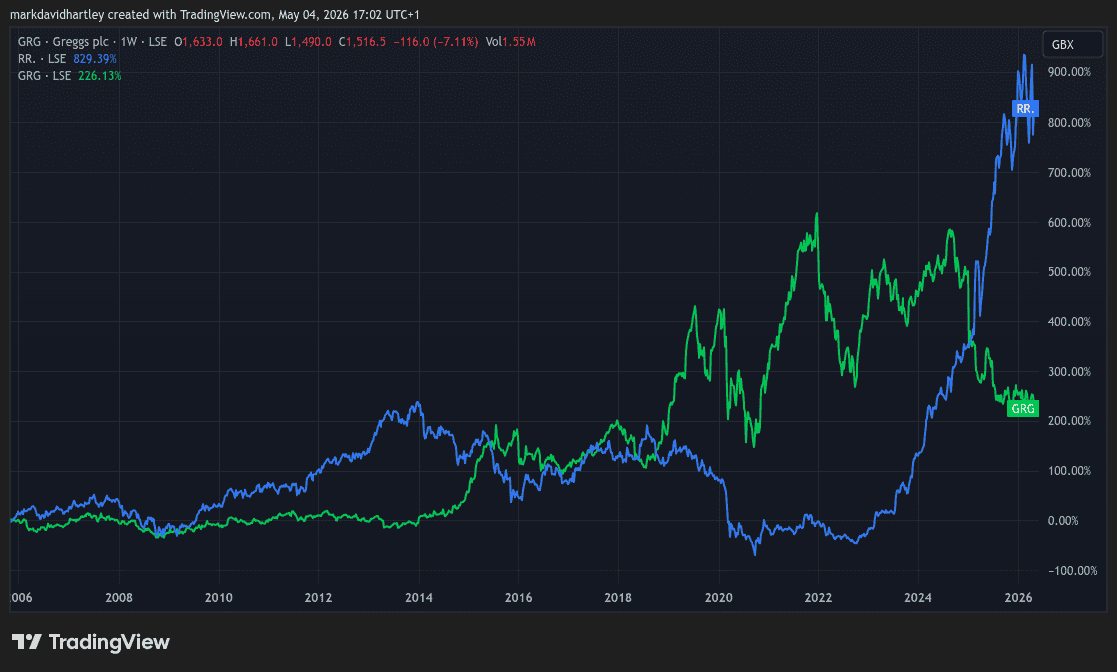

Currently trading at around £15 each, Greggs (LSE: GRG) shares have lost more than half their value since 2022 peaking at more than £33.

A shocking comparison to the promising growth stocks that once existed in the late 20s. And that’s why it symbolizes the price function of Rolls-Royce between 2010 and 2020.

So is it possible that Greggs could do a complete 180 and collect huge dividends over the next five years?

Let’s take a closer look.

Big challenges

The similarities between Gregs today and Rolls-Royces of yesteryear run deeper than just the share price.

In both cases, the sharp decline was largely driven by external factors. In Rolls’ case, the Covid-19 pandemic halted air travel around the world. For Greggs, changing consumer habits and increasing income have been very profitable.

But we don’t know that the success of Rolls involves returning the flight only, otherwise all flights will have the same luck. CEO Tufan Erginbilgiç’s role in the recovery cannot be understated, which is where Greggs begins to doubt.

Can Gregg CEO Roisin Currie, who is up for 2022, help the bakery make a Rolls-like recovery?

Why Gregs recovery is visible

There are several factors at play in the story of Gregs strong recovery. Most notably, it still has strong fundamentals and cash flow.

It is seen as a leading brand of ‘food to go’, with strong like-for-like sales, and a pipeline to open new stores and formats (railroad, mall, supermarkets).

After its sharp fall from the highs of 2021, analysts now describe it as ‘cheap’ compared to earnings and monetization. The current price is only 12 times the estimated future earnings.

That’s good for a consumer protection business, simple. As costs come down, management now aims for a return on operating income (ROCE) of around 20%. So even a small margin improvement could re-rate the shares.

That means the 20-year-old growth narrative could return in full — if external problems ease.

But will it be a Rolls-like recovery?

Although I have hope for Greggs, I also look at the facts. Roll’s 1,000%+ rally came from moderate balance sheet reform, double-digit margin expansion, and extensive government spending on defense.

Greggs is different because it is a smaller, more cyclical, consumer-competitive stock. It does not exhibit the same structural strength and explosive strength.

Add to that ongoing challenges like the cost of living crisis, climate-sensitive foot traffic, and changing eating habits, and it faces a tough future.

I think it is reasonable to expect growth in the range of 300%-400% over the next five years if conditions improve and trends change.

But there is little chance of either FTSE the stock will match Rolls’ performance once within a decade.

An important point

Arguably the UK’s most popular bakery chain, Gregg’s has grown significantly since 2020. Between 2020 and 2025, it has increased its store count from about 2,000 to over 2,700.

But rapid expansion may occur prematurely. After the Labor government introduced budget reforms in October 2024, the company faced the threat of rising costs.

And yet despite these ongoing risks, it has managed to maintain a healthy balance sheet. Shrinking margins are a concern but cash flow growth and an attractive advice to measure recovery potential.

The future may be uncertain, but for value investors optimistic about the UK economy, Greggs is a compelling option to consider.