The energy shock in 2022 is a sign of a possible disappointment for the investment market in 2026 as the war in Iran continues, writes writer Chris Duncan.

The escalating war in Iran has pushed oil prices to their highest level since 2022. That was not a good year for investors. Are we destined for a repeat in 2026?

Continued inflation is the biggest fear. Markets are already moving quickly to lower interest rates. The Bank of England, which was expected to break 50 basis points on the bank rate this year, now looks set to hike.

Two-year gilt yields reacted favorably, rising to 4.10% from 3.52% before the crash. The 10-year yield has reached 4.79%, up nearly 60 basis points.

The US fared slightly better. The US Dollar Index – which has spent much of the past 12 months weakening, angering non-dollar investors in US assets – is now trading above 100, having posted two consecutive weekly gains. Its strength amid fading expectations of rate cuts helps explain why gold, among the safe havens that have embarrassed the crisis, has been such a wet squib.

That doesn’t mean all US goods escaped unscathed. Treasury bonds across the board have sold off since the start of the war, albeit by much smaller degrees than in the UK. The equity market has been resilient.

The S&P 500 fell about 3% during the crisis, a surprisingly muted reaction to the lack of visibility during the supply disruption, one of the largest in oil market history.

Strong corporate earnings and a strong US economy are said to explain the sanguine response. However, updated figures last week showed that the US economy grew at an annual rate of 0.7% in the fourth quarter of 2025, half of the original estimate.

Yes, the US Government shutdown was a big draw. But the strong rebound this quarter can be attributed to a slowdown in consumer spending, a trend that won’t be helped by higher pump prices.

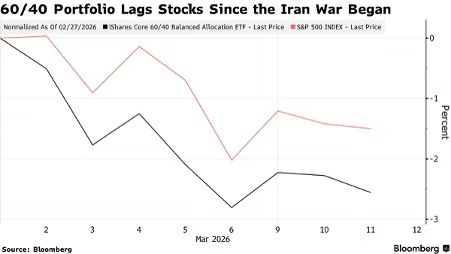

With stocks and bonds both lower — and central banks facing stagflation, their worst case scenario — investors in balanced portfolios could face yet another painful year.

In 2022, stocks and bonds are moving popularly in lockstep, with one significant correlation coefficient between those asset classes hitting 0.92 (with +1 indicating a positive overall correlation). Today, that rate is even higher.[1]

How bad things get from here depends on how long the disruption lasts. Iran’s Supreme Leader Mojtaba Khamenei says he wants to keep the Strait of Hormuz closed.

US strikes on military bases on Kharg Island, a key hub for Iran’s oil exports, have not eased tensions. JPMorgan analysts said a strike on the Kharg oil fields would “immediately halt the bulk of Iran’s crude exports, potentially triggering severe retaliation in the Strait of Hormuz or against the region’s energy infrastructure”.

If major damage occurs to that infrastructure, it will increase the time for oil and gas prices to rise, leading to global inflation.

The glass full argument is that there is a major difference between now and 2022. US interest rates were close to zero in March of that year, when the US CPI was 8.6% (and Brent Crude was trading above $125).

Today, the Fed’s policy rate is 3.5%-3.75% and the US CPI is 2.4%. Although US markets have dismissed interest rate cuts – now not expected until the end of 2026 at the earliest – long-term inflation expectations remain below 3%. The yield is much higher than it was in 2022. Covid, unlike then, is a distant memory.

However, the conflict has disrupted some of the businesses that were doing well at the beginning of the year. Many investors had placed a weak dollar and strong emerging markets. The dollar’s sudden rally has complicated that bet, especially as rising energy costs put more pressure on developing economies, which are now unable to lower interest rates.

Meanwhile, markets such as South Korea, home to chip juggernauts Samsung and SK Hynix, experienced wild swings, with the KOSPI falling 12% in a single day in early March, its biggest drop on record.

It could be worse. With traditional safe havens offering limited protection, strategists have floated a number of alternatives, from Chinese stocks to uranium.

Asset managers such as Invesco argue that investors should hedge risk by increasing exposure not only to oil and gas, but also to other commodities transported through the Strait of Hormuz, such as aluminum and ammunition. Yet conservative portfolio managers say there is little they can do, other than reduce risk and wait for more clarity.

Political situations can end quickly, and stock markets deliver good years after major conflicts.

But if inflation rises or stays higher for months rather than weeks, the crisis could re-emphasize the lesson learned in 2022: high inflation means traditional portfolio diversification offers less protection than investors expect.

[1]

")