People have been debating the so-called “loan equity ratio” for years now.

It is also known as the gold handcuffs of extremely low interest rates that make it difficult to move.

On the other hand, you have this below-market mortgage rate and the associated cheap mortgage payment.

On the other hand, it makes it difficult to give up that level if/when you sell, so you can stay put, even if you don’t want to.

Now there is a new system where you get a carrot; the main discount if you offer that sweet price.

Can You Give Up Your Low Mortgage Rate To Reduce Principal?

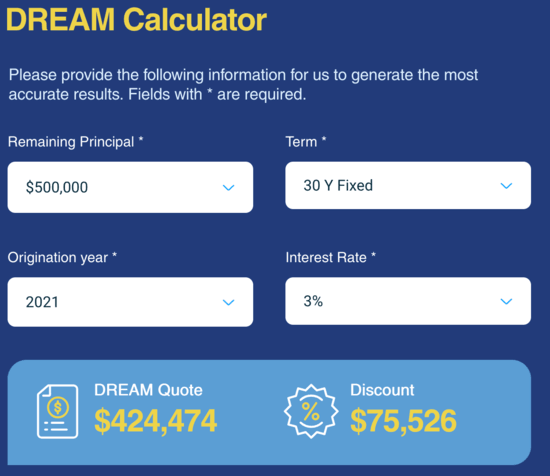

Imagine you have this 2.75% 30-year fixed rate loan that you took out in 2021. It still has a balance of $500,000 and your payment is incredibly low.

You wanted to move because your family is growing, or just because you don’t like your home anymore. Maybe there is a job opportunity in a different city.

The problem is that today’s house prices look very different. If you sell and lose that 2.75% fixed rate, you could be looking at a 6.50% rate. Wow!

This is a real problem that many existing homeowners are facing due to the ZIRP era, followed by a series of Fed rate hikes and rising bond yields, driven by inflation.

Just look at the chart above from the FHFA’s National Mortgage Database (NMDB). Nearly two-thirds of California homeowners have a mortgage rate of 3.99% or less!

Sure, they can sell for a pretty penny on what they paid, but a replacement home is more expensive too.

We’ve seen both house prices and mortgage rates rise in tandem, in a way that many believe is inversely related.

The New DREAM Program Can Make Travel More Attractive

Enter the DREAM program from a fintech company called Takara.

It stands for Discount for Real Estate Affordability and Mobility, and as the name suggests, it offers a deal to existing real estate sellers willing to sell.

Not only is the problem of closing the mortgage rate for owners, it also means that there is less property for sale to prospective home buyers.

So this gets the housing market moving again, hopefully, by removing the “penalty” of offering a very low mortgage rate.

The way it works is straightforward. The lender gives the borrower a discount if he sells and repays the loan early.

While you keep hearing that myth that banks don’t want you to pay off your loan early, it couldn’t be further from the truth with loans for the 2020-2021 season.

Those are sitting on a bank balance somewhere, which drives them crazy while the markets are in some cases more than double that.

And if they stay there for another 25 years, it will be very painful for investors.

To reduce that, you agree to sell, give up your rate, and take a new loan at today’s rates.

In return, you get a discount “that can reach 10% or more of the loan balance.”

As seen in this screenshot, the discount can be quite large, totaling $75,000 on a $500,000 loan balance.

In other words, the bank pays off $75,000 of your loan if you pay off the loan early.

Then you need to decide if it’s worth giving up that low amount (and very low interest charges) so you can move.

That’s Why I Say Thinking Before Voluntarily Paying Off A Cheap Loan

There are all these posts on the internet about how to pay off a loan early.

And how much they saved. But what is the opportunity cost? Can that mortgage “investment” be transferred elsewhere?

If you willingly agree to pay off a 2-3% loan early, you are essentially locking in a 2-3% return on investment.

Doesn’t sound so good does it? Especially when stocks are going up in double digits, and even an old savings account is earning 3-4% these days.

The fact that banks are willing to pay you to pay off a cheap loan early tells you everything you need to know.

Before creating this site, I worked as an account manager for a real estate broker in Los Angeles. My experiences in the early 2000s inspired me to start writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the mortgage process. Follow me on X for the hottest.